Welcome

Long-Term Capital Appreciation

LTCA Objective: Disciplined long-term capital appreication through the capture of equity market beta and augmented with attractive individual alpha-generating opportunities.

LTCA Holdings: Approximately 25-30 individual stocks, benchmark aware (US Equities) in terms of market sectors and capitalizations.

Portfolio:

How to use this information:

Sortable Headers: Click a header to sort the table by that metric.

Tgt. Wgt. (LT-Rating): This value is the target holding weight within the portfolio, and collectively they add up to 100%. This value also serves as a long-term rating. Specifically, this is a compelling enough position to hold in that particular weight for the long-term (or until something fundamental changes about the holding).

1D%: This is the price change for the most recent trading day.

52W: This is the current price as a percent of the 52 week high and low price range (the high and low price are listed at the right and left side of the progress bar).

Rating (Near-Term): Short-term market noise can drive share prices above or below their long-term value. Shares generally don’t make it into the portfolio on near-term ratings alone (they have to be long-term compelling), however near-term ratings can create compelling opportunities to add shares and/or rebalance portfolio weights.

Buy Under: This is the price at which it can make sense to purchase shares from a valuation standpoint. The percent above or below the current share price drives the near-term ratings.

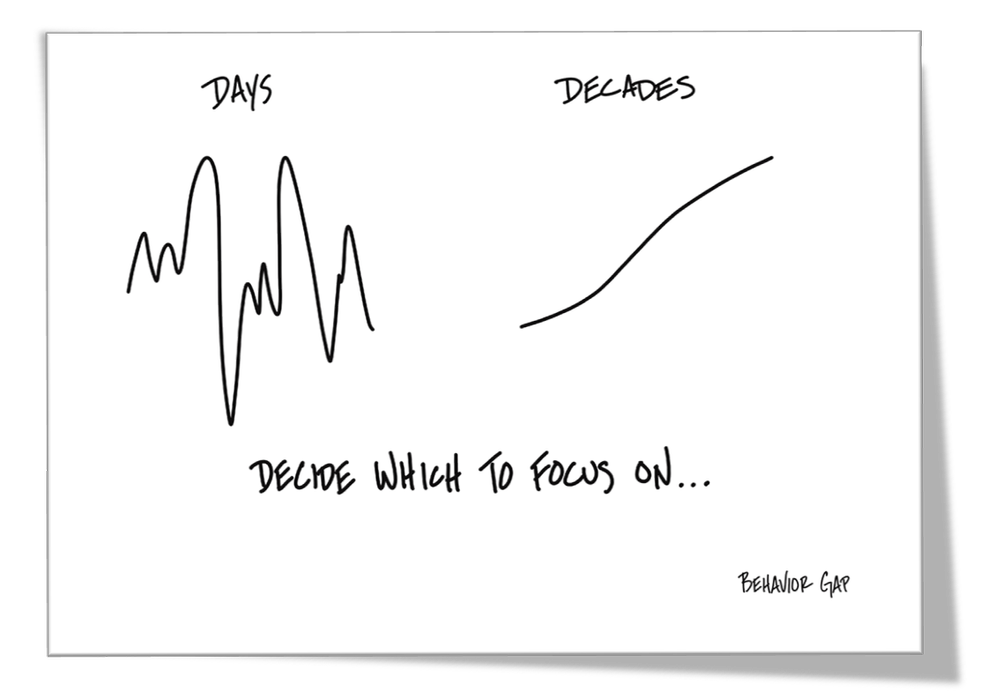

Why long-term capital appreciation: Often hidden in plain sight by the siren songs of the fear-mongering media, long-term compound growth is one of the most powerful wealth-creation machines in the history of the world.

You may have heard the children’s story, if I gave you a penny on day one, and then gave you double the amount each day thereafter…

1 penny on day one

2 pennies on day two

4 pennies on day three

8 pennies on day four…

…how long would it take you to become a millionare?

Speaking in pennies may not sound like much, but incredibly, it would take less than one month to become a millionaire (not too long!) …and to a certain extent—that’s a great framework for understanding the incredible power of long-term compound growth. In recent decades, the S&P 500 has been doubling every six or seven years!).

Every day some media headline will tell you the sky is falling—and they will try to make you “panic sell” all your stocks—but if you can hold on for the long-term—despite any near-term volitlity—compound growth eventually kicks into high gear—and so too does your wealth.

In fact, one of the main reasons passive ETFs (such as a basic S&P 500 index fund) beats the pants off so many investors in the long run, is simply because it imposes the discipline (no panic-selling, no market timing, no unreasonable concentration) that long-term compound growth—unmolested by fear—is able to work its powerful “magic!”

CIO Vantage: Risk Management

LTCA Sector Exposure:

For risk management purposes, investors may choose to keep sector exposures similar to an index—unless they feel particularly strong about an individual sector’s opportunities. This helps control performance deviation risks from sector drift, and can work as a hedge against unknowable macroeconomic risks (e.g. new government regulations, commodity prices, consumer and technology shifts) that may impact a particular sector’s performance (positively or negatively).

The goal isn’t necessarily to match index sector weights, but to be aware of them and the risks they may expose investors to.

CIO Vantage: Risk Management

LTCA Market Capitalization:

Similar to sector risk exposures, market cap exposures pose risks that should be monitored. For example, small caps tend to be more domestic (less international) in their revenue generation, and geopolitics can cause them to perform better or worse at certain points in the economic cycle.

The goal isn’t to match the market cap weights versus an index or benchmark, but rather to be aware of the risks they pose, and to allocate your individual “risk budget” accordingly.